Iraq

Iraq United Arab Emirates

United Arab Emirates Saudi Arabia

Saudi Arabia Bahrain

Bahrain Kuwait

KuwaitEnglish

Iraq Pharmaceuticals Market Opportunities

Over the past few years, political and security conditions in Iraq have improved significantly, which led to significant growth of the Iraqi economy, driven mainly by increase in oil exports. Over the next 5 years, Iraq GDP is estimated to grow at a CAGR of 8.3%, reaching ~US$ 200b by 2018. However, Iraq healthcare sector is significantly lagging behind MENA region.

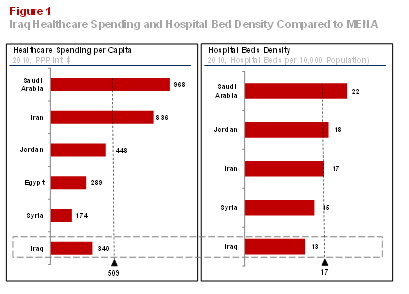

In terms of annual healthcare spending per capita, Iraq is lagging behind the MENA region. Compared to a MENA average of US$ ~510, Iraq healthcare spending per capita in 2010 was only US$ 340 (see figure 1). In terms of healthcare infrastructure, Iraq is also lagging behind MENA. For example, while MENA region had an average of 17 hospital beds per 100,000 capita, Iraq had only 13 hospital beds per 100,000 capita (see figure 1).

Given the current state of healthcare sector in Iraq and the significant projected economic growth, healthcare sector in Iraq is expected to grow significantly. Among the different segments of healthcare, pharmaceuticals market in Iraq is expected to grow significantly.

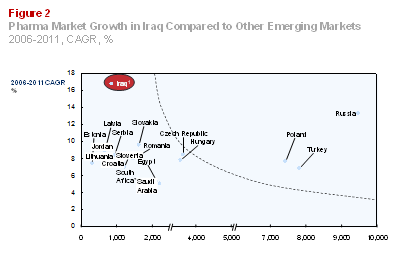

Iraq’s pharmaceuticals market has experienced unparalleled growth over the period 2006-2011

Over the past few years, Iraq pharmaceutical market has experienced fast growth, both on the generic and originator drugs segments, compared to other developing markets. Among similar markets in Eastern Europe, Middle East and Africa, Iraq had the highest growth in pharmaceutical market over the period 2006-2011, with ~17% CAGR (see Figure 2).

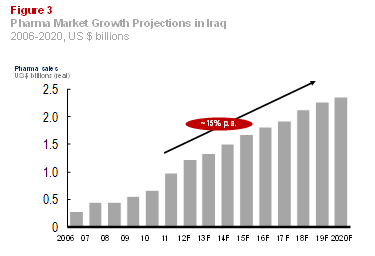

Industry reports expect Iraq pharmaceuticals market to continue its healthy growth till 2020

According to Business Monitor International (BMI), Iraqi Pharma market is forecasted to grow by 10-15% annually over the next seven years. As shown in figure 3, Iraq pharmaceuticals market is expected to reach US $ ~2.4 billion by the year 2020.

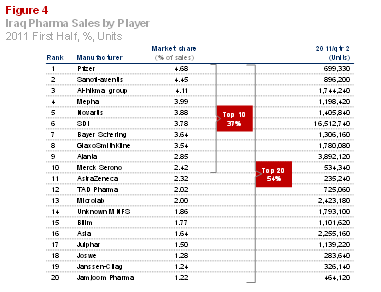

The Iraqi pharmaceutical market is fragmented with no dominant players

Compared to global industry trend, Iraqi Pharma market is rather fragmented. During 2011 first half, sales of top 10 Pharma players in Iraq accounted for only 37% of the total sales, compared to a global average of ~60%, while sales of top 20 players accounted for only 54%of the total sales, compared to a global average of ~80%, as shown in figure 4.

Along the drugs distribution chain in Iraq, several types of entities exist that differ in role

In Iraq, drugs can be purchased from different entities, depending on the volumes, including manufacturers, scientific offices, distributors/large drug stores (Madkhar), and small drug stores (Madkhar).

Manufacturers: drugs manufacturers are the actual producer of the drugs. Purchase of drugs directly from the manufacturer is only applicable for large volumes.

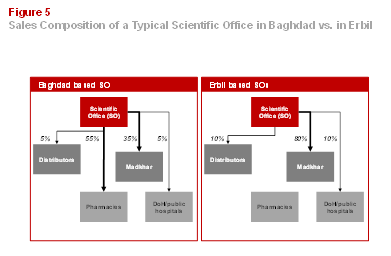

Scientific Offices: a scientific office is the sole distributor of an imported drug, thus each type of drugs has one scientific office, chosen by the manufacturer. The scientific office imports the drug from the manufacturer and distributes it to distributors, drug stores and hospitals. The customer portfolio of scientific offices in Iraq differs based on geography. For example, while scientific offices in Erbil make 80% of their sales to drugstores (Madkhars), scientific offices in Baghdad sell ~55% of their sales directly to pharmacies and only 35% to Madkhars (see figure 5). There are about 250-300 scientific offices in Iraq.

Distributors/Large Drug Stores (Large Madkhar): Distributors and large Madkhars are companies that trade in large volumes of several drugs. Those entities buy drugs from scientific office in large volumes and supply it at smaller quantities, usually to Madkhars and public hospitals/health directorates. There are 125-150 distributors/large Madkhars, with average monthly drug purchase of ~ IQD 300 million US$ 250k).

Small Drug Stores (Small Madkhar): Madkhar is a drug store that basically buys drugs from distributor/large Madkhar or scientific office and supplies them to public and private hospitals, and pharmacies. There are 125-150 Madkhars.

Iraq has 3 main customer segments that differ in size and procurement model

Currently, the drug market in Iraq is composed of three different segments; two are public sector and one is private sector.

Ministry of Health (MoH): Through the State Company for Marketing Drugs and Medical Appliances (KIMADIA), MoH purchases drugs directly from manufacturers, due to large volumes, and distributes them to public hospitals and primary healthcare centers, through the governorate’s directorates of health. The estimated value of KIMADIA annual drug purchases is between US$ 400 million and US$ 600million.

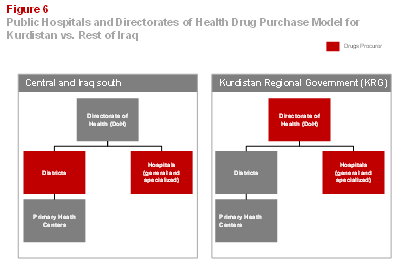

Public Hospitals and Directorates of Health:As KIMADIA drug purchases do not cover all of the public hospitals and primary healthcare centers’ needs, public hospitals and directorates of health procure additional drugs, each on its own, from either scientific offices, distributors or Madkhars,

depending on the quantity and availability. The purchase authority differs between Kurdistan and rest of Iraq. In the Kurdish region, the directorate general of health procures drugs and distributes them to primary healthcare centers, through districts’ directorates of health. In rest of Iraq, these additional drug purchases are more decentralized, with the district directorates of health purchasing drugs to supply primary healthcare centers, while public hospitals purchase their drugs needs on their own. Figure 6 depicts the difference in public hospitals/primary healthcare centers’ procurement model between Kurdistan and rest of Iraq.

The estimated aggregate value of public hospitals and directorates of health’s annual drug purchases is between US$ 150 million and US$ 250million.

Private Hospitals, Clinics and Pharmacies: Private hospitals, clinics and pharmacies procure drugs individually, mainly from drugstores (Madkhar), which buys drugs from either scientific offices or distributors. The estimated aggregate value of private hospitals, clinics and pharmacies’ annual drug purchases is between US$ 600 million and US$ 900million.

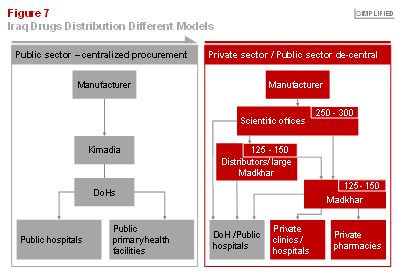

The different models of drug distribution in Iraq are shown in figure 7. The left box outlines the central KIMADIA procurement chain, while the right box illustrates the decentralized purchases of drugs by public hospitals, health directorates, private hospitals/clinics and private pharmacies.

Lack of reliable/recent market information and low penetration of electronic PoS systems remain the major obstacles for success in the Iraqi market

Given its current size and growth potential, the Iraqi pharmaceuticals market is one of the most promising ones in the region. However, the lack of reliable pharmaceutical market information, especially for the private market, represents a major disadvantage. Moreover, the little/ no penetration of electronic Point of Sales systems makes the collection and processing of sales information extremely difficult, thus discouraging many international Pharmaceutical manufacturers from stepping-up their activities in Iraq, e.g., by setting up their own import/sales infrastructure or even manufacturing facilities. Therefore, creating reliable drug sales data for the private market through regular pharmacy audits will be a crucial component to create the necessary visibility and transparency that international Pharma companies would require if they would increase their “commitment” to the Iraqi market.

In order to successfully grow the Iraqi market, international pharmaceutical companies need to address multiple strategy elements

To achieve success in the Iraqi market, several strategic elements needs to be addressed:

Balanced strategy between public and private market segments: Given that the Iraqi market is almost equally divided between public customers (both KIMADIA and the drug purchases of individual hospitals and health directorates) and private customers, pharmaceuticals companies need to develop a market strategy that is balanced between both sectors and takes into account the key differences, e.g. sales approach, procurement process, and drug portfolio.

Long-term public sector supply contracts: As private sector market fluctuates, in terms of volumes and prices, pharmaceuticals companies in Iraq should aim at securing long-term supply contracts with key government clients, mainly KIMADIA, health directorates and major public hospitals.

Securing reliable agent with required reach: As distribution of imported drugs in Iraq takes place through scientific offices, picking the right scientific office to distribute company’s products is mission critical to the manufacturer’s success in Iraq. While selecting the scientific office(s), the manufacturer should consider several factors including, but not limited to, the scientific office’s geographical footprint, its customer portfolio (i.e., distributors and Madkhars), its sales volumes, both to private and public sector customers, its track record in drug distribution, and the size and quality of its sales force.

Creating own high performing sales team: To ensure continuous success and maximum market penetration, pharmaceuticals companies should consider building their own sales and marketing team in Iraq that ensures continuous promotion of the company’s products and monitoring of sales levels for company’s products and competitor drugs.

Management Partners is a top-management consultancy advising leading private and public sector institutions from the US, Europe and the Middle East, with a particular regional focus on Iraq, UAE, and Saudi Arabia. The consultancy firm assists clients across industries in areas such as designing growth strategies, implementing operational performance measures and providing market intelligence through on-ground research.

Featured Videos

Featured Articles

»

»

»

»

»